Ladder Life Insurance Review: Best Bet for Term Coverage?

By Ben Carter

9.2

Consumer's Best Score

Consumers Best Verdict: Ladder Life (Broker/Platform) Highlights

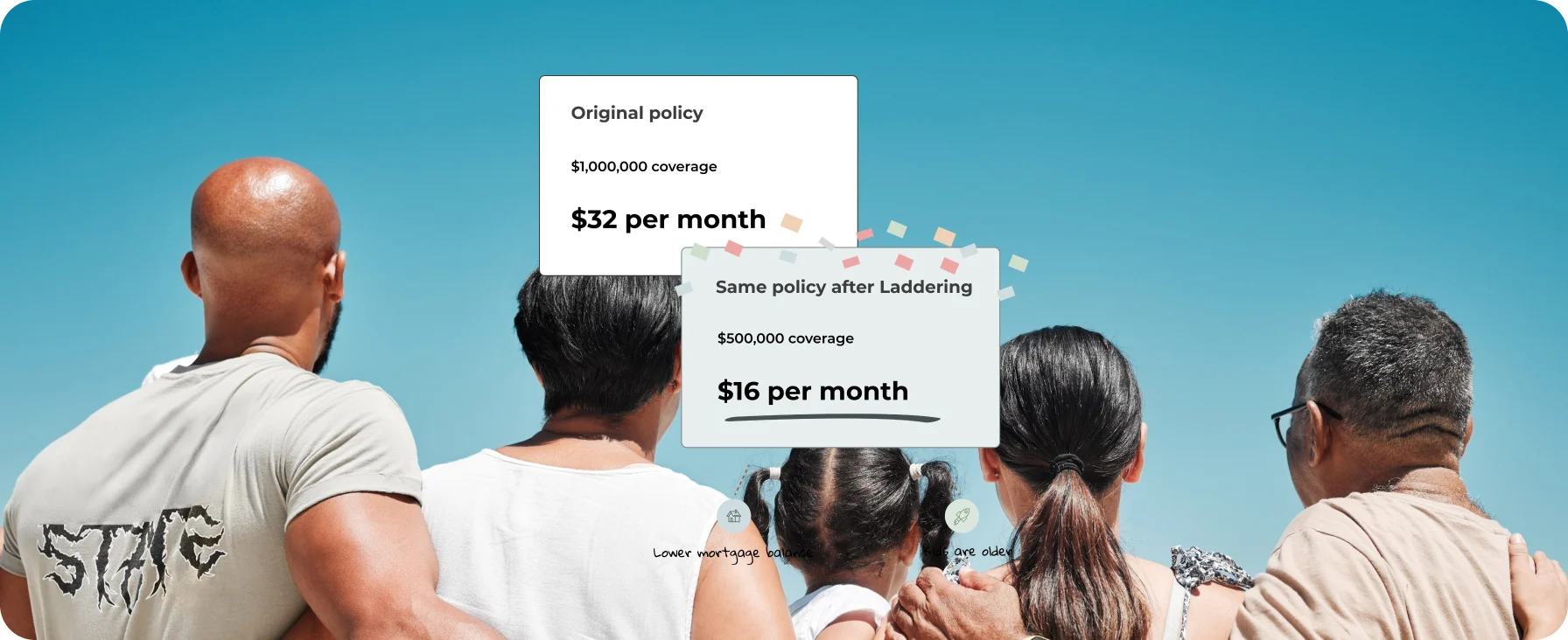

In this ladder life insurance review, we found a platform built for speed and simplicity. You apply online, often get an instant decision, and manage everything from your phone: beneficiaries, payments, and—here’s the hook—coverage adjustments as life changes. It’s term-only, with limited add-ons, but that clarity is part of the charm. Think: dependable, no-fuss protection you can actually tweak when your needs shift.

After living with it, poking at it, and yes, trying to break it a little, my take is simple: Ladder Life (Broker/Platform) nails the modern term-life experience. It’s fast, mostly exam-free for many applicants, and the ability to dial coverage up or down later is genuinely useful—not just marketing fluff. Pricing is sharp for healthy folks, and the digital interface is refreshingly straightforward. It’s not a fit if you want permanent life insurance or a bunch of riders, but for clean, flexible term coverage, it’s a standout. If you’re even mildly curious, I’d run a quick quote—it takes a minute and clears up a lot.

In-Depth Look: Ladder Life (Broker/Platform) Features & Considerations

Core Features & Consumer Benefits

Here’s what stands out once you move past the homepage and into real-life use.

Instant, fully online application

Get a quote in seconds and a decision in minutes—no appointments, no paper shuffling.

Flexible coverage you can adjust

Lower your coverage (and premium) anytime, or request an increase when life gets busier—weddings, babies, mortgages.

Often no medical exam

Many qualified applicants can skip labs, which means faster coverage without the wait.

High coverage potential

Competitive rates for healthy applicants with the option to go up to multi‑million limits if you qualify.

Clear, minimal product lineup

Term-only means fewer confusing choices and transparent pricing without sneaky riders you don’t need.

Important Considerations & Potential Downsides

- Term-only product

No whole or universal life options, and limited rider choices compared to traditional agents.

- Not everyone skips the exam

Larger coverage amounts or certain health histories may still require medicals.

- Age and state limitations

Availability, term lengths, and maximum coverage can vary; older applicants may have fewer options.

- Digital-first service

Great for DIY shoppers, but those wanting a dedicated local agent or in-person reviews may feel underserved.

Who Is the Ladder Life (Broker/Platform) Best For?

Busy professionals

You want solid coverage without meetings—apply on your lunch break, done.

Young families

Budget-friendly term now, with room to boost coverage when life (and kids) happens.

DIY, tech-comfortable shoppers

Prefer clear, self-serve control over a salesy agent experience.

High earners with big obligations

Need multi-million coverage for mortgages, income replacement, or business needs.

People whose needs will change

Plan to scale coverage down later as debts shrink and savings grow.

Who Might Want to Explore Other Options?

- Permanent-life seekers

If you want cash value or lifelong coverage, look at whole or universal life instead.

- Rider-heavy planners

If you need extensive riders (e.g., robust disability waivers, child riders), a traditional carrier may fit better.

- Older or complex-health applicants

A specialized broker who can shop multiple underwriters might secure better terms.

- Hands-on advisor fans

If you want in-person guidance and annual sit-down reviews, a local agent model may feel more comfortable.

Frequently Asked Questions

Make Your Savings Grow Faster.

UFB Direct, a division of Axos Bank, offers a high-yield savings account designed for individuals looking to maximize their interest earnings with minimal fees. It's an online-only option focused on providing competitive rates and a straightforward banking experience.